Mapping Range Construction Principles from Heads-Up Battles onto Milestone-Based Retirement Contribution Adjustments

Range construction in heads-up poker involves narrowing an opponent's possible holdings based on betting patterns, position, and prior actions while simultaneously refining one's own range to maintain balance and exploit imbalances, and this same narrowing process applies directly to milestone-based retirement contribution adjustments where individuals refine savings rates at specific life stages such as career promotions, home purchases, or family expansions. Observers note that both systems require continuous reassessment because static ranges or fixed contribution schedules fail when new information arrives, whether that information comes from an opponent's check-raise or from updated market volatility data released in early 2026.

Core Elements of Range Construction in Heads-Up Play

Heads-up battles force players to assign precise probabilities to hand combinations because every decision carries immediate feedback, and researchers studying decision theory at multiple universities have documented how elite competitors build ranges by combining board texture analysis with opponent tendencies observed across thousands of hands. Data from tournament tracking services shows that successful heads-up specialists adjust their continuation betting frequencies by as much as 18 percent when facing opponents who defend wider on earlier streets, demonstrating that range construction is never a one-time exercise but an iterative process updated after each action.

Those who study poker mathematics emphasize that range construction also accounts for blockers and unblockers, meaning certain cards in a player's own hand reduce the likelihood that an opponent holds specific combinations, and this blocker concept transfers cleanly to retirement planning where existing assets such as vested stock options or inherited accounts reduce the urgency of aggressive contribution increases at later milestones. In May 2026, several financial education platforms began incorporating these poker-derived frameworks into their planning tools, citing improved user engagement when contribution schedules were presented as dynamic ranges rather than fixed percentages.

Translating Range Principles to Retirement Milestones

Milestone-based retirement systems trigger contribution adjustments at predetermined life events, yet the effectiveness of those adjustments depends on how accurately an individual constructs the range of possible future market and income scenarios, much like a heads-up player constructs an opponent's range before deciding whether to call a river bet. When a person reaches age 40 or receives a significant salary increase, the appropriate response is not a uniform percentage hike but a recalibration that weighs current portfolio allocation, projected healthcare costs, and tax law changes against the probability of each outcome.

Case studies compiled by retirement research centers indicate that individuals who treat contribution decisions as range refinements rather than binary choices achieve higher median account balances by retirement age, primarily because they avoid over-committing during high-volatility periods and under-committing when conditions stabilize. The mapping becomes especially useful when external shocks occur, such as unexpected tax code revisions or sector-specific downturns, because the same logic that tells a player to tighten their range after facing multiple three-bets also tells a saver to pause aggressive increases until more data clarifies the new environment.

Practical Application Steps

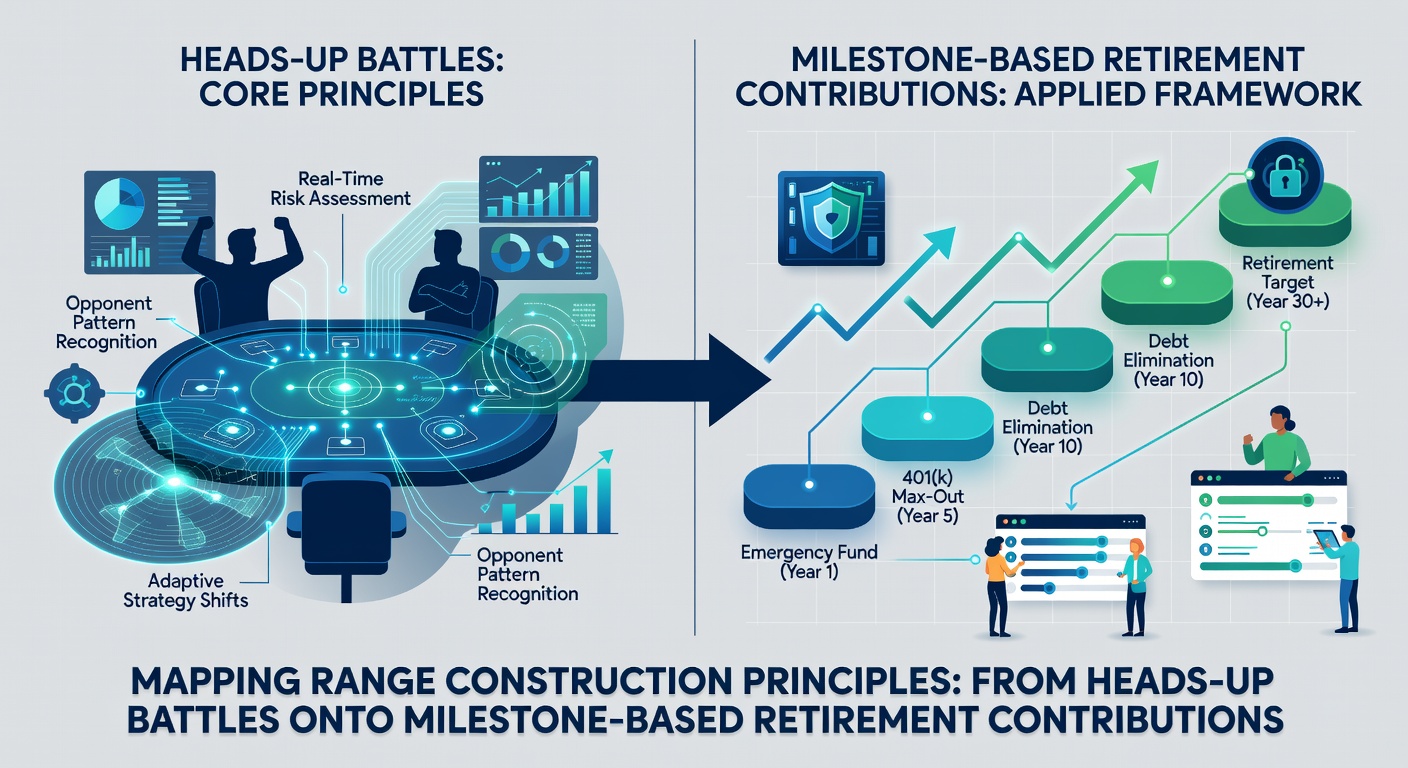

Experts recommend beginning the mapping process by listing all relevant variables that affect contribution capacity, then assigning probability weights similar to how poker solvers assign frequencies to hand categories, and this structured listing prevents emotional reactions that often distort both poker decisions and financial planning. Next comes the identification of blockers, which in retirement terms include existing pensions, real estate equity, or spousal income that narrows the range of additional savings required at upcoming milestones.

Regular review intervals mirror the street-by-street adjustments made in heads-up play, with many practitioners scheduling portfolio and contribution reviews every six months or after major life events, and data from longitudinal studies of retirement savers confirms that those adhering to scheduled reviews maintain contribution rates within 3 percent of optimal targets more consistently than those who review sporadically. Software platforms that integrate poker-derived range visualization tools have reported increased user retention rates, particularly among professionals already familiar with strategic decision frameworks from competitive gaming.

Conclusion

The transfer of range construction principles from heads-up poker onto milestone-based retirement contribution adjustments provides a coherent framework for handling uncertainty because both domains reward precise probability assessment and timely refinement over rigid adherence to initial plans, and organizations tracking retirement outcomes continue to gather evidence that this cross-domain approach yields measurable improvements in long-term financial positioning when implemented consistently.